Introduction

One lever is to make it less costly to employ workers. Critics of Keir Starmer’s government have pointed to rises in employer’s social security contributions (national insurance contributions (NICs)), national minimum wages and increased regulation through the Employment Rights Act (ERA) as all contributing to these increased costs. There are good arguments for increasing national minimum wage and for many of the measures in the ERA, but this article does not consider the pros and cons of these changes.

Raising employment costs through higher employer NICs is another matter. The government may be right in needing to increase tax revenue but there are other ways.

As job opportunities for many become scarcer, particularly for younger workers, this article considers whether moving in the opposite direction and reducing or even eliminating a tax on employment would be prudent.

Below, I look at the history of taxing work in the UK and the available evidence of the impact of cutting employer NICs. I reflect on whether it is realistic to reduce significantly or eliminate taxes on employment and how the UK compares with other countries. I conclude by looking at two countries which do not tax jobs materially – Denmark and New Zealand and the lessons which might be gleaned from these economies.

Background

Most countries generate tax revenues from similar sources – an individual’s income (whether from work, profits or gains); corporate profits; sales of goods and services (VAT); and a levy on employers for employing people (employers’ social security contributions (SSCs - NICs in the UK). These sources are broadly accepted by populations as legitimate (even if the amounts levied can be contentious) and have evolved over time. In the UK income tax goes back to the 18th Century; sales taxes to 1940; and employer’s NICs to the National Insurance Act of 1911.

NICs (including those paid by the employee as well as the employer) originally funded an individual’s health and welfare benefits.

Though NICs are still paid into a National Insurance Fund to pay fund many welfare benefits, NICs have become indistinguishable from general taxation receipts as any surplus can be used to reduce government debt and any shortfall is topped up from general tax receipts (employee NICs are really now an additional income tax even if the rules of application do differ in some cases from income tax).

The post-Industrial Revolution world of work relied heavily on manpower (and it was predominantly male). Offshoring, automating or insecure alternatives to employment were rarely realistic options. The service (tertiary) sector only comprised 55% of the workforce in 1966 increasing to around 84% (and increasing) fifty years later as manufacturing, construction, agriculture and mining jobs disappeared. Taxing work in those days made much more sense at a time when alternatives to employing people to do work were less available.

The world has changed a lot over the last century or so. Businesses now have alternatives to employing employees in the UK which they wouldn’t have had in past decades – the potential to automate jobs which is forecast by many to increase dramatically with AI and robotics and result in large numbers of job losses; moving jobs overseas is more realistic than it used to be; and ways around costly employment through the gig economy and other forms of self-employment have become more common.

A lot of money is raised for the Treasury’s coffers from employers’ NICs. In the UK 9% of tax receipts are generated from this source. This amounts to about £108 billion per year - sums and percentages which the Office for Budget Responsibility have forecasted to increase over 2025/26 and in subsequent years. Replacing this (even if it was partly offset by a boost to economic growth) would make Rachel Reeves’ £22 billion black hole seem very small.

Recent changes

The April 2025 rise in the headline rate of employers’ NICs from 13.8% to 15% grabbed the media attention but another change was also very relevant in that the lower limit for employers’ NICs fell from £9,100 to £5,000 capturing many lower paid part-time employees – though one benefit of which was to remove the incentive on employers to restrict lower paid workers to low hours contracts.

Fifteen percent is the highest rate for employer NICs in recent times as the rate has fluctuated between about 10 and 14% over the last half century leaving aside the short-lived health and social levy in 2022.

The 2025 changes were accompanied by an extension of the Employment Allowance in both value and scope which reduced somewhat the impact of the increased levy for many employers but the increased costs were nonetheless significant.

Business organisations as well as businesses themselves, particularly labour-intensive ones such as retail and hospitality and particularly those hit hardest by increases in National Minimum Wage rates, were very critical of this increase and the impact it would have on employment. A CIPD survey a year ago found that a third of respondents reported an intention to reduce hiring or make redundancies because of rising employment costs including increased employer NICs (though some may exaggerate the foreseen impact of changes they oppose).

Reducing employers’ NICs – studies

Our recent Future@Work 2026 report shows that, globally, UK-based employers are the most concerned about the impact of legislation on taxation and employer contributions on workforce planning and policy, with approximately one in four identifying this as the principal regulatory challenge.

If the UK were to reduce or even eliminate employer NICs, it would seem intuitive that employers would employ more people or increase the hours of existing employees reducing underemployment.

In 2009 the OECD highlighted work undertaken in Austria modelling cutting employer SSCs for low paid workers (20% of workers) and concluded it would raise overall employment levels by 0.4% and GDP by 0.3%.

A 2021 IFS study looking at the impact of reduced employer SSCs in Hungary in older and younger workers concluded that for higher productivity businesses which tend to hire from competitors the impact of cutting SSCs is to increase pay whereas for lower-productivity employers who hire the unemployed, the impact is increased employment. This further supports cutting or eliminating employer NICs to combat increasing unemployment.

Implications of reducing or eliminating employer NICs

The studies referred to above confirm the assumption that cutting the tax on employment would increase employment both in numbers and in the hours offered to part-time workers. They also show that increased employment boosts a country’s GDP.

Seeking to draw lessons from the Austrian study which only modelled the impact on the economy of cutting employer SSCs for the 20% lowest paid employees, cutting it for all workers would, by extrapolation, increase employment and growth further.

However, even, say, a 1% increase in GDP in the UK would only generate £10 billion in additional tax receipts (assuming the percentage of GDP received through tax receipts remain stable). This would be a small fraction of lost revenue from eliminating employer NICs. Most of the lost tax receipts would have to come from somewhere else and we see the uproar which follows any modest rise in other taxes.

There would be other benefits to reducing or eliminating employer NICs. There would be an increase in income tax and employee NICs arising from increased employment. Increased income would generate increased consumption and an increase in revenue from consumption taxes. Following the Hungarian study above, even if in some cases the reduced employment cost was passed on in higher pay, these benefits would follow.

Increased employment would reduce welfare payments. More people in work would generate health benefits and, as well as the NHS savings, would result in less financially tangible benefits such as improved mental health and self-worth and the sense of purpose and belonging which can come from meaningful employment.

Comparison with other countries and over time

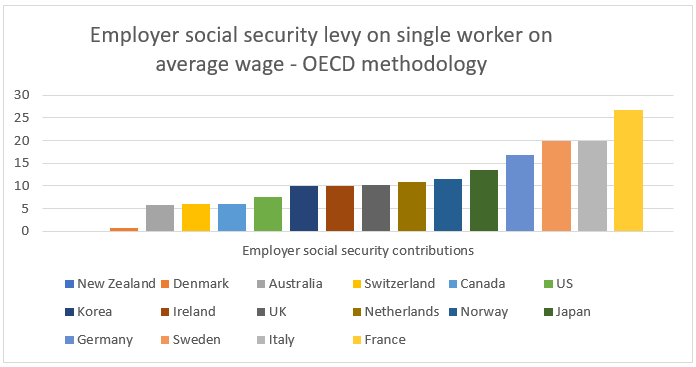

UK employers’ NICs are not out of line with competitor economies. Most (but not all countries) do tax work. It is clear that some other countries such as Australia, New Zealand, Denmark and the US do not tax work or tax it at much lower rates than the UK. Others, however, such as France and Germany tax work much more highly that us.

These direct comparisons are not easy as the level of workplace, retirement or unemployment benefit funded directly or indirectly by employer contributions varies from country to country. In some countries the level of contributions varies by region.

By way of example of these complexities, Australia has no federal employer social security contributions. States and territories do however levy employer contributions, e.g. New South Wales at 5.45% but only on larger employers. Australia, like some other countries, requires that mandatory employer contributions must be paid to fund pensions for employees (superannuation contributions in Australia). In many respects these can be equated to the employer contributions British employers have to make to individual pension schemes to match voluntary employee contributions. However, Australian superannuation is more comprehensive, and the state pension means tested. As a result, one could argue that employer superannuation contributions Down Under do, in part, fund payments which are met out of general taxation in the UK (the state pension).

Using the methodology used by the OECD, the UK, even with the recent increase in employer NICs, is around mid-point for taxing work.

Denmark

Keir Starmer’s Labour government turned to Denmark and the success Matte Frederiksen’s centre left government has had in combatting the populist right with robust immigration policies. They could do worse than reflect on Denmark’s approach to taxing work to boost the British economy. Denmark’s tax on work is negligible.

In Denmark, there are no general employer social security contributions, but Danish employers must make various contributions which are hypothecated to fund payments such as maternity leave payments and short-term unemployment payments (which are generous in Denmark and form part of their much talked about “flexicurity” approach).

These payments are generally a fixed sum per employee rather than a percentage of gross pay. Again, we need to take into account variances between the different schemes as state-funded Danish maternity pay is paid at 80% of salary for 12 months. UK state-funded maternity pay is much lower, but many employers elect to pay more generously – payments funded in Denmark out of employer contributions.

Comparing total tax revenues in the UK and Denmark, Denmark generates most of its revenue from taxing individual’s income, profits and gains whereas the UK gains more from taxing employment and from property taxes.

| Income tax/employees SSCs/CGT | Employers SSCs | VAT | Corporation tax | Property taxes | Fuel duty | Alcohol and tobacco | IHT | |

| UK | 40% | 9% | 21% | 9% | 11% | 2% | 2% | 1% |

| Denmark | 57% | 1% | 21% | 8% | 4% | 3% | 2% | 1% |

The makeup of a country’s tax receipts should not, however, not to be confused with the level of taxation. Denmark is well-known for its high taxes, but this is a different debate from how tax receipts should be sourced.

Denmark taxes more heavily than any other OECD member (45% of GDP) whereas the UK (34%) is at the average amongst OECD member states (notwithstanding the claims that the country is highly taxed as this is by reference to historical numbers not to comparisons with other countries).

New Zealand

Another interesting comparison is with New Zealand which does not tax employment at all. It manages to do this whilst generating only 42% of tax receipts from taxes on personal income, profits and gains (only a slightly higher percentage than the UK).

Whilst Denmark concentrates on more highly taxing income, New Zealand concentrates more highly on consumption.

VAT in New Zealand contributes a higher percentage of the total (29%) than the UK or Denmark (both 21%) with corporation tax generating 13% and property taxes 6% (between the UK and Denmark’s approach in each case). VAT is, however, charged at 15% in New Zealand (though the turnover at which a trader must start charging VAT is much lower in NZ than in the UK and the base is much broader than here with fewer exempt goods or services) and corporation tax is 28% (higher than the UK or Denmark).

New Zealand generates taxes amounting to 33% of GDP (so similar to the UK).

Conclusion

As automation increases the pressures on employment, questions about the wisdom of taxing jobs (or, at least, taxing them so heavily) will only grow.

Employers’ NICs generate over £100 billion for the UK exchequer so replacing any lost revenue would not be straightforward and increasing other taxes whether on income or consumption or otherwise would inevitably be greeted with howls of protest. Nonetheless, in our changing world, there may be little alternative but to use the levers available to mitigate against these pressures on employment.

Employment is a good thing and taxing it seems counterintuitive. Societies tax activities they wish to discourage and relax taxes on activities to be encouraged. Additional taxes are levied on alcohol, smoking, gambling, sugary drinks and second homes. Taxes are relaxed on saving for retirement, donating to charities or corporate investment in research and development.

It is true that most countries do tax jobs and many more heavily than the UK does. However, looking at two countries which do not, the alternatives are plain – the Danish model where an individual’s income, profits and gains are taxed more heavily or the New Zealand model where consumption is taxed more heavily.

The UK can learn from both and whilst reducing dramatically or eliminating the tax on jobs may seem unrealistic today, it is a journey government should start on by setting out long-term ambitions and prioritising cuts to employers’ NICs as soon as tax cuts are being considered. Targeted reductions are also worthwhile considerations. The widely reported difficulties young people face in finding first jobs and work more generally could be mitigated by reducing employer NICs on the employment of say under 24 year olds.