Remuneration regime: consultation on material risk takers

29 September 2021

The Prudential Regulation Authority is consulting on changes to the identification of material risk takers for banks, building societies and PRA-designated investment firms

Overview

On 8 September 2021, the Prudential Regulation Authority (PRA) launched a consultation on three proposed changes to the requirements on identification of material risk takers (MRTs). These requirements are applicable to banks, building societies and PRA-designated firms including third-country branches – collectively referred to as CRR firms

The three elements of the consultation

In summary, the PRA is proposing to:

- Change the Remuneration Part of the PRA Rulebook to insert the criteria for identifying MRTs derived from Capital Requirements Directive (CRD) V and the European Banking Authority’s draft regulatory technical standards (RTS) published on 18 June 2020 – the final version of which was published in broadly similar terms on 9 July 2021 (MRT Regulation).

- Update its Supervisory Statement 2/17 to reflect the rule changes described above and a revised process for excluding an employee from being identified as a MRT solely based on quantitative criteria (see below).

- As a consequence, revoke the previous RTS issued in March 2014 which originally set out the criteria for identifying MRTs.

It is worth noting that the PRA is proposing to redenominate the currency of the remuneration thresholds from EUR to GBP at a rate of £1 = €1.14.

Who are MRTs and why is this important?

Broadly speaking, CRR firms must identify their MRTs in order to apply the requirements of the Remuneration Part of the PRA Rulebook.

MRTs’ remuneration is subject to stringent requirements, including on the ratio of fixed to variable remuneration (the so-called bonus cap) and calculation of those elements; deferral of variable remuneration; malus and clawback; and restrictions on guaranteed variable remuneration and buy-out awards. In some circumstances, variable remuneration may be rendered void and recoverable if it does not comply with certain remuneration rules. For further details see our Inbrief guide Remuneration Codes - For banks, building societies and investment firms.

How are MRTs identified?

The identification of MRTs is not straightforward. An employee is identified as a MRT on the basis of:

- Qualitative criteria – where the employee’s professional activities have, or are deemed to have, a material impact on the firm's risk profile. Employees in firms not subject to the Remuneration Part should be included as MRTs if their activities pose a risk to the CRR consolidation group or directly to a CRR firm.

- Quantitative criteria – where the employee’s total remuneration in the preceding financial year is significant, unless the firm is able to show that the employee’s activities do not in fact have a significant impact on the risk profile of a material business unit.

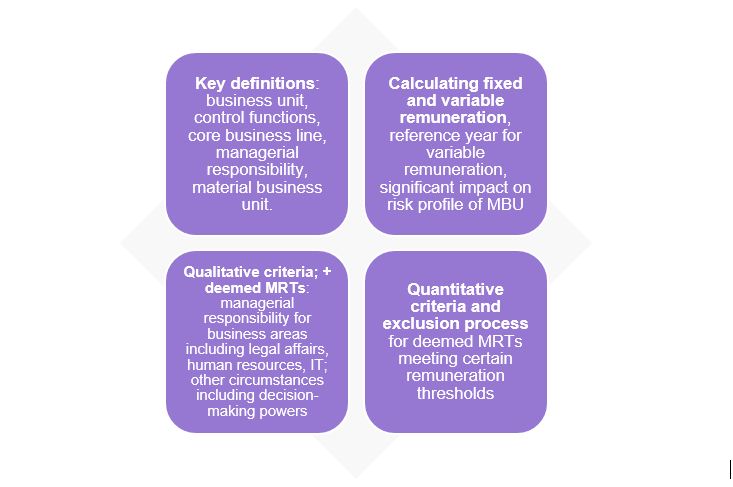

The MRT Regulation clarifies how to identify MRTs, and how to apply the remuneration requirements to MRTs once identified. Key areas covered by the MRT Regulation include:

The qualitative criteria under the MRT Regulation include some additional roles where an employee will be deemed to be a MRT, such as:

- Employees with managerial responsibility for: the soundness of accounting policies and procedures; prevention of money laundering and terrorist financing; information security; and a function’s (material) outsourcing arrangements.

- Employees with authority to take, approve or veto decisions on credit risk above a certain threshold.

The MRT Regulation has also provided some welcome clarity on the meaning of certain terms including control function, business unit and material business unit. The latter has been widened to include any unit that could generate material profits, revenues or franchise value for the firm or create a material prudential risk.

As the MRT Regulation emphasises, however, the qualitative criteria set out in the MRT are not exhaustive and firms are still required to carry out their own analysis to ensure that any employees who create material risks are identified as MRTs.

The quantitative criteria have been simplified. Unless an exclusion is obtained, an employee will be deemed to be a MRT if one of the following applies:

- The employee’s total remuneration in or for the preceding performance year is at least £440,000 and equal to or greater than the average remuneration awarded to members of the firm’s management body and senior management.

- The employee’s total remuneration in or for the preceding performance year is at least £660,000.

- Where the firm has over 1,000 employees, if the employee’s remuneration is within the 0.3% of employees within the firm who have been awarded the highest total remuneration in or for the preceding performance year.

There will no longer be a freestanding quantitative criterion capturing employees as MRTs where their total remuneration in the preceding financial year is equal to or greater than the lowest total remuneration awarded in that financial year to a member of senior management.

The PRA is also proposing to revise the process for excluding employees from being MRTs if they have been identified solely on quantitative criteria. While additional clarity is provided in terms of the process, the bar to be met before employees are excluded from being MRTs may be higher as there is now a specific obligation on the PRA to ensure that its objective of promoting the safety and soundness of PRA-authorised persons is satisfied. It remains to be seen whether in practice the PRA excludes fewer employees as MRTs under the new process.

What happens next?

The deadline for responding to the consultation is 8 November 2021, with implementation from the first performance year starting after publication of the final rules. This is currently intended to be in Q4 2021. If you have any comments on the PRA’s proposals, please let us know.